Asset-Based

Lending

Asset-based lending comes in many forms from invoice factoring to equipment purchases. We offer a variety of solutions for today's small business owners. Leverage assets owned by your business. Asset-based lending includes non-debt options as well as debt facilities.

Invoice Factoring

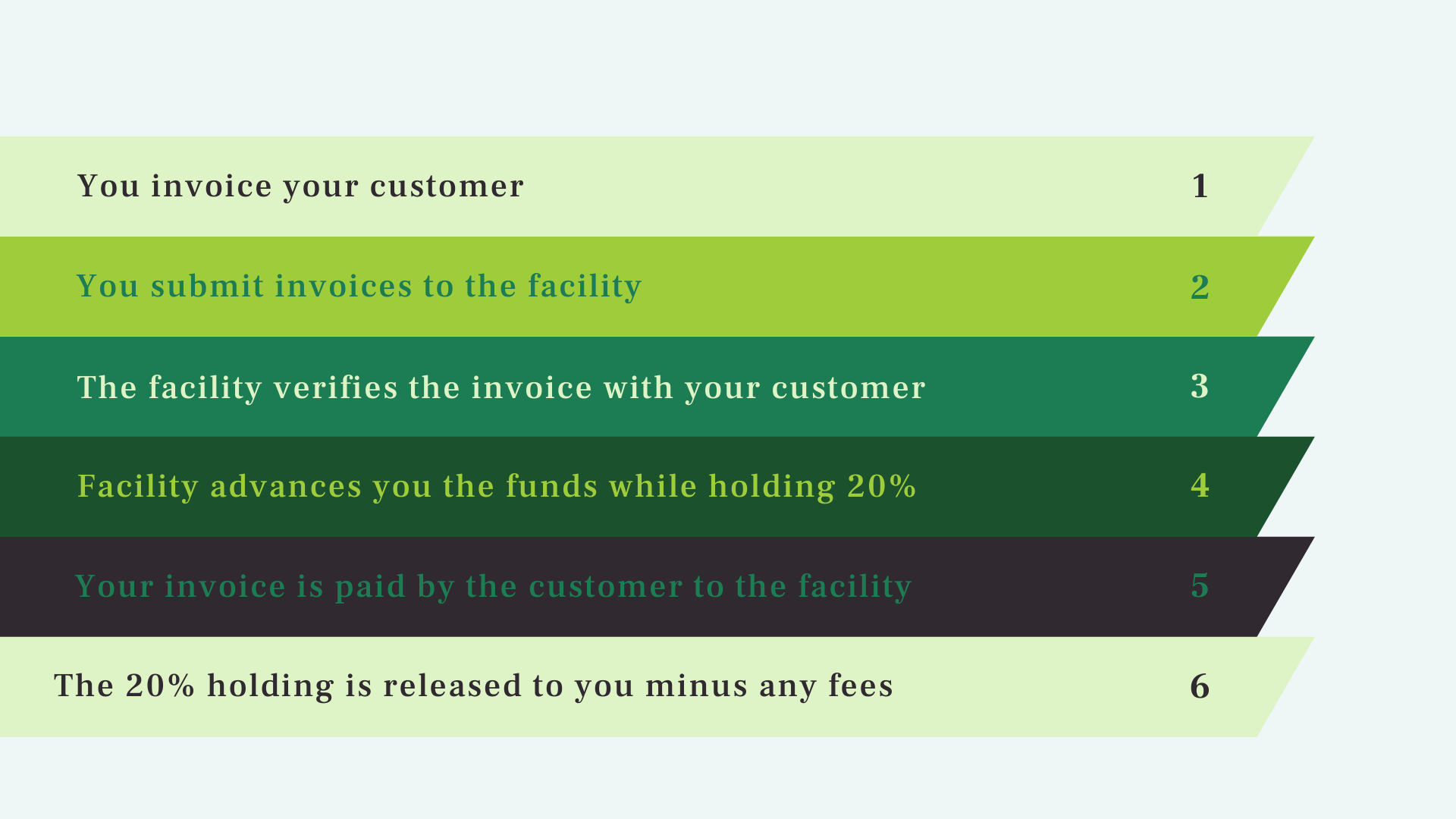

Invoice factoring is a cost-effective solution to cash flow issues. Companies grossing $3,000,000.00 annually often begin to have cash flow issues as growth begins to outpace liquidity.

The factoring facility underwrites your customers to make sure they have the ability to pay the invoice. Once your customers are approved you remit invoices to the factoring facility. Once the invoice has been verified, 80-95% of the invoice is released to you directly while the remaining amount is held until your customer pays the invoice.

Once your customer pays the invoice the remaining amount is released to you, minus any fees. Fees are assessed in buckets. For example, on a NET 30 invoice, you will pay a 1-2.5% fee. For NET 31-60 days, an additional fee percentage is added, until the invoice is repaid.

- An invoice factoring facility is the BASE of any specialty ABL financing including P.O. Financing and Government Contract Mobilization

- FICO - Any, however, you must bill b2b

- Industry types who find this useful, Medical, staffing, construction, transportation, suppliers, wholesalers, manufacturing, oil and gas, solar, distributors

- Cons - Customer must verify invoices

- Pros - Cost-effective, supportive for growth

Some facilities allow you to “age” your invoices before submission. IF you have a customer that you know pays on net 90 terms, you have the ability to hold the invoice for 60 days until your fee structure would be the NET 30 bucket. You can look at an invoice factoring facility as a way of extending credit to your customers and include fees in your billing if you would like. This makes Invoice factoring one of the cheapest ways to avoid borrowing and continue to support healthy grow

We are here to answer your questions

Sign up for a consultation to talk through your funding options. Our account managers are skilled in helping business owners navigate the many options available on today's marketplace.

Asset-Based Line Of Credit

Our asset-based line of credit program is perfect for business owners who own property, have a large Accounts receivable portfolio and own equipment. A credit decision is reached by placing a loan to value or LTV on each asset. Accounts receivable LTV is taken from an average of the current and previous ledgers. And generally will reach somewhere around 90% LTV. Property is currently being collateralized at 65-80% depending on the lender and an average LTV for equipment depending on condition and what the equipment is generally is around 65% LTV but may be lower.

An Asset based LOC is commonly found in two forms, a ledgered line or a non ledgered line.

Both Invoice factoring and sales ledger facilities advance up to 85% of the submitted invoice

Both Invoice factoring and sales ledger facilities advance up to 85% of the submitted invoice, ledger lines offer flexibility for companies that have outgrown a traditional factoring facility but still need access to capital due to delayed receivables. Often ledgered lines can turn into a more traditional ABL line or eventually a true business line of credit. Ledgered lines are available for companies doing a minimum of 4 million dollars annually, with accurate and stable financials.

Asset Based lines which are not ledgered, do not require you to submit or verify invoices or transactions. There will be a static base number of wha t your AR is worth along with other assets and a credit line will be released based on that information. Depending on the lender rates can range from 8- 36% with an average around 18%

A ledgered line requires at the minimum monthly audits of invoices and documentation, and submission of sales ledgers. How this differs from factoring, is mainly just what it is called. However there are few key differences to note. One being that not every invoice will have to be verified by your billed customer. But you can expect some if not most to be, Lenders love security. it is more expensive than invoice factoring coming in around 8-30% depending on the lender. Where an average rate for an invoice facility for a net 30 term is 2.5%

Equipment Financing

Equipment financing refers to two different programs, Acquisitions and Leasebacks.

If you are looking to purchase equipment for your business, financing can be accessed for acquiring equipment. Alternately if you own valuable equipment and are looking to lien the equipment for working capital, you may be eligible for what is called an Equipment Leaseback program.

Equipment leaseback programs are helpful if you own valuable equipment and would like to leverage it as security for a collateral loan, without putting a blanket lien on all business assets, much like with an SBA loan.

Personal credit must be 640 or a cosigner is needed. Leasebacks value equipment at the “fire sale value” or, the value of the equipment if there was a forced liquidation in the event of default. The LTV or Loan to Value of equipment leasebacks is on average 65%.

Equipment Financing is available for equipment purchases. Terms are 3,5,7 years with a low monthly payment. It is helpful to have a model number or purchase in mind when applying. The bank may set limitations on the age of equipment only financing newer models.

Asset Based Lending

Leverage assets & accounts receivable for growth liquidity

@ Copyright 2020 - Simplified Funding Solutions | All rights reserved

646.403.4992

admin@simplifiedfundingsolutions.com